(co-author: Ken Dai)

Healthcare has consistently ranked among the top enforcement priorities for Chinese antitrust regulators, reflecting its direct implications for consumer welfare and public policy. In recent years, the State Administration for Market Regulation (“SAMR”) has intensified scrutiny of the sector, including high-profile enforcement actions against anti-competitive conduct in active pharmaceutical ingredients (APIs), finished drugs, and medical devices. Between 2022 and 2024 alone, authorities imposed a series of penalties across these segments, underscoring that healthcare remains a “red-line” industry for competition enforcement in China.

Merger control represents an equally important pillar of enforcement. In addition to determining whether individual deals may restrict or eliminate competition, merger review provides a useful perspective on broader industry dynamics, including patterns of consolidation and the regulatory considerations involved. Recent transactions have spanned the full value chain—from pharmaceuticals to devices, distribution, and healthcare services—and frequently involve both vertical and mixed elements. An examination of cases reviewed between 2022 and 2025 sheds light on prevailing deal trends, market definition practices, and the areas of regulatory focus most relevant to companies pursuing healthcare investments in China.

I. Transaction Types and Representative Transactions

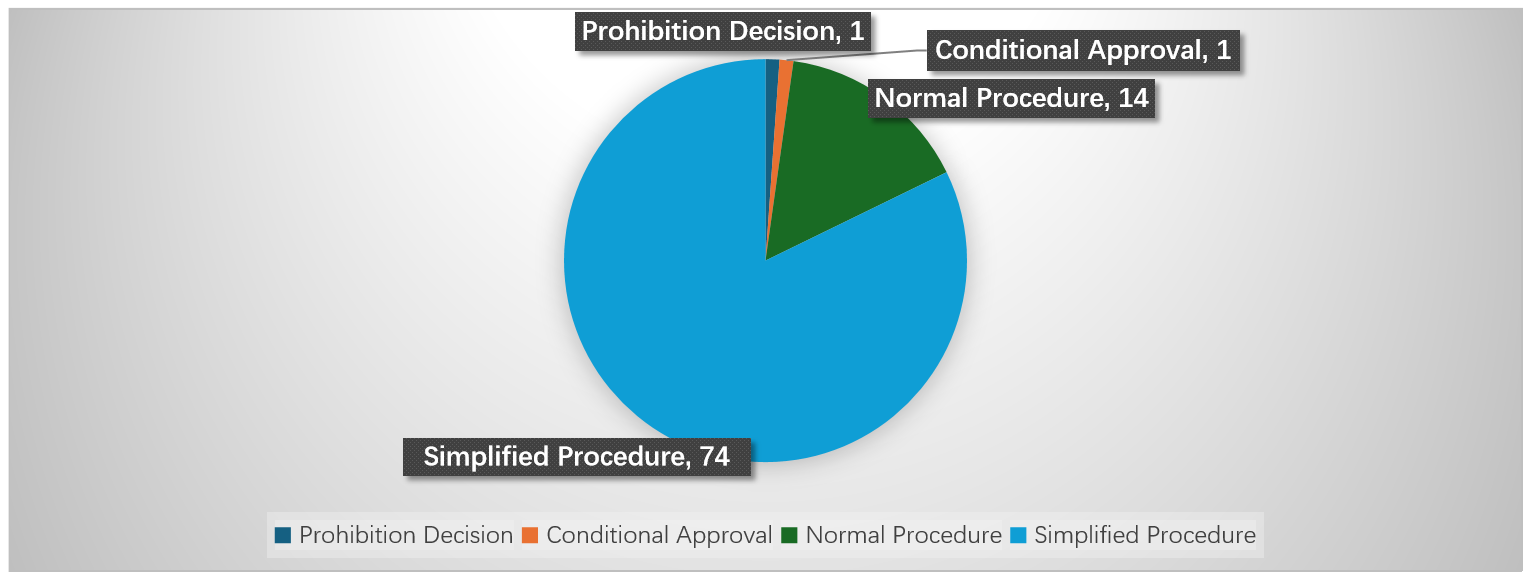

From January 1, 2022, to August 11, 2025, SAMR concluded 90 merger review cases in the healthcare sector, covering biopharmaceuticals, medical devices, healthcare services, and pharmaceutical distribution. Of these, one transaction was cleared with conditions, one was prohibited, and 88 were unconditionally cleared. Among the unconditional clearances, 14 cases were reviewed under the normal procedure and 74 under the simplified procedure, with simplified cases accounting for over 80% of the total. On average, the review period was approximately 19 days, indicating that review efficiency in this sector has remained relatively stable.

Two cases that did not receive unconditional approval are noteworthy. The first is Simcere Pharmaceutical’s acquisition of Beijing Tobishi Pharmaceutical, which marked the first instance in China where a below-threshold transaction was voluntarily notified and approved subject to conditions. The case is also significant as it represented the first time a Chinese court conducted a full substantive review of SAMR’s merger decision, setting an important precedent for judicial scrutiny. The second is Wuhan Youtong Pharmaceutical’s acquisition of Shandong Beida Gaoke Huatai Pharmaceutical, where SAMR launched an ex officio review six years after the deal had closed and ultimately prohibited the transaction, ordering the parties to unwind the deal and terminate exclusive distribution arrangements. These two cases illustrate the regulator’s willingness to expand the scope of intervention and highlight the heightened compliance risks facing market participants in the healthcare sector.

(i) Changes in Transaction Structures and Case Volumes

In terms of transaction structures, equity acquisitions remain the predominant path for consolidation in the healthcare sector. Among the unconditional approvals, 67 cases involved equity acquisitions, 4 involved asset/business acquisitions, 1 involved control through contractual arrangements, and 16 were new joint ventures. Joint ventures were more commonly seen in R&D collaborations, value chain extensions, or regional market expansion.

Case volumes have fluctuated over the past three years. Both 2022 and 2023 saw 27 cases each, representing a relatively high level of activity. In 2024, the number fell slightly to 24 cases, and in 2025 (through August 11) only 11 cases had been concluded, noticeably fewer than in previous years. This fluctuation reflects not only the deal-making pace of merging parties but also broader financing conditions in the sector. Public data show that in 2024, China’s healthcare industry recorded 1,465 primary market financing deals, down 26.75% year-on-year, with total investment falling by 10.4% to RMB 73.7 billion. This illustrates the continuing “capital winter” facing Chinese biopharma and healthcare firms, which in turn has dampened merger activity.

At the same time, government policies are being introduced to stimulate industry consolidation. In late 2024, Shanghai issued an Action Plan (2025–2027) to support M&A by listed companies, including the creation of a RMB 10 billion biopharma M&A fund. In April 2025, Beijing announced measures to support innovation in the pharmaceutical sector, including a RMB 50 billion industry fund and a RMB 10 billion dedicated M&A fund. The interplay of capital market conditions and policy support will likely be a key determinant of future deal volume and transaction structures in the healthcare sector.

(ii) Key Market Participants

Since 2022, merger cases in China’s healthcare sector have shown distinct patterns among participating parties. Leading domestic companies such as China Resources Pharmaceutical, Fosun Pharma, Tongrentang, and Mindray have remained central to consolidation, expanding through both horizontal and vertical transactions. State-owned groups, including Sinopharm, China General Technology, and China Traditional Chinese Medicine, have been particularly active in distribution, healthcare services, and medical devices. Multinational pharmaceutical companies have played a dual role—strengthening their presence via joint ventures (for example, AstraZeneca’s collaboration with Shenzhen Kangtai on RSV vaccines) while divesting non-core businesses to local firms or funds (such as Roche’s sale of oncology drugs Xeloda and Tarceva). At the same time, investment funds like CBC Group, Carlyle, KKR, Warburg Pincus, and Advent have been prominent, both as buyers of divested assets from multinationals and as drivers of consolidation across retail pharmacy chains, specialty hospitals, and biotech startups.

(iii) Representative Transactions

Several transactions over the past three years stand out for their industry significance and antitrust implications. China Resources Pharma completed successive acquisitions of stakes in Kunming Pharmaceutical and Tasly, both horizontal deals in the traditional Chinese medicine (TCM) and specialty drug segments. These transactions strengthened China Resources’ position in cardiovascular treatments and increased market concentration in key therapeutic areas. China General Technology’s acquisition of Neusoft Medical marked the entry of a central SOE into the high-end imaging equipment sector, reflecting vertical integration from healthcare services into digital medical device manufacturing, with potential long-term impact on domestic competition in advanced equipment. Tongrentang Group was frequently involved in transactions, forming joint ventures or acquisitions with partners such as China Resources Runyao, Jointown, and Haoyaoshi, thereby expanding into distribution and retail channels—a strategy likely to reshape regional competition. Another notable case is ByteDance’s acquisition of Amcare Healthcare, which signaled the expansion of internet platforms into offline specialty hospital services. The transaction prompted concerns over whether platform advantages in data and traffic could translate into market power in high-end medical services.

II. Case Distribution and Market Definition

(i) Transactions Focused on Supply Chain Integration and Cross-Sector Expansion

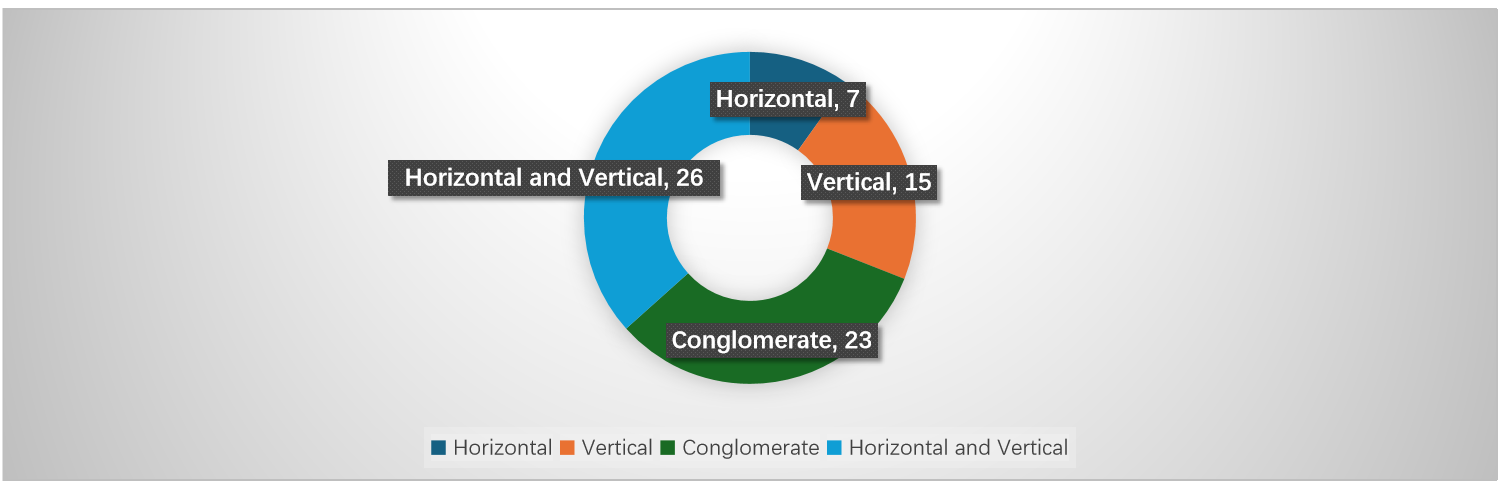

Simplified procedure cases in the healthcare sector since 2022 show that, purely horizontal mergers accounted for only 7 cases, while 15 involved vertical relationships, 26 combined both horizontal and vertical elements, and 23 were classified as mixed transactions. Unlike traditional manufacturing industries—where horizontal overlaps dominate—healthcare mergers tend to feature more complex vertical and cross-market dynamics.

Two factors help explain this pattern. First, the healthcare value chain is highly fragmented, spanning R&D, manufacturing, distribution, retail, and service delivery. Companies often pursue vertical or mixed integration across these stages to optimize supply chains and strengthen market positioning. Second, the rise of new business models—such as internet hospitals, third-party diagnostic services, and healthcare IT systems—has brought additional cross-sector elements into transactions, producing cases where horizontal overlaps coexist with vertical dependencies.

(ii) Predominance of Transactions in the Formulated Drug Market

By transaction type, the formulated drug segment—including chemical drugs, traditional Chinese medicines, and certain biologics—has accounted for roughly 60% of healthcare merger cases since 2022. This reflects the continued concentration of M&A activity in specialty drugs, generics, and TCM, which remain core areas of China’s pharmaceutical industry.

Approximately 25% of transactions involved distribution and healthcare services, covering wholesale and retail pharmacies, hospitals, clinics, internet hospitals, and healthcare IT systems. These cases often exhibited vertical links with upstream formulation businesses. The medical device segment, including imaging equipment, in-vitro diagnostics (IVD), electrophysiology, and interventional consumables, represented just over 10% of transactions. By contrast, the active pharmaceutical ingredient market appeared only in isolated cases (e.g., heparin sodium), and remains a relatively minor part of merger control activity in this sector.

(iii) Relevant Market Definition: Product Markets Defined by Indications and Categories; Geographic Markets Diverge Upstream and Downstream

The Anti-Monopoly Guidelines for the Pharmaceutical Sector (the “Pharmaceutical Guidelines”), issued by the State Council’s Anti-Monopoly and Anti-Unfair Competition Committee set out the framework for defining relevant markets in this sector. In line with general substitution principles, product market definition must also account for the industry’s particularities, including the intended use or therapeutic effect (indication), route of administration, product characteristics, physician and patient preferences, and the impact of regulatory or reimbursement policies. On the supply side, factors such as production capacity, technological barriers, and intellectual property protection are also considered.

The Guidelines provide differentiated approaches for specific segments. Active pharmaceutical ingredients are typically treated as separate product markets due to their unique role in drug manufacturing. Chemical formulations may constitute individual markets if they lack substitutes for specific indications. Traditional Chinese medicines are assessed with reference to factors such as raw material sourcing, brand recognition, and entrenched prescribing or consumption habits.

Geographic market definition is likewise differentiated. For manufacturing and distribution, the relevant market is generally defined as China-wide, reflecting uniform regulatory and licensing standards. By contrast, R&D and innovation activities may be assessed on a global basis, while retail and distribution services—such as hospital and pharmacy sales—may be confined to specific regions or cities, reflecting local patient catchment areas and reimbursement arrangements.

In recent merger review practice, the principles outlined in the Pharmaceutical Guidelines have been widely applied and further refined in specific cases:

A. Definition of Relevant Product Market

Information disclosed in simplified procedure cases shows that product markets in the pharmaceutical sector are typically defined by therapeutic function. For drugs, markets are commonly segmented by therapeutic area or functional attributes—such as cardiovascular, respiratory, gastrointestinal, anti-infective, and immunosuppressive treatments—covering both chemical formulations and traditional Chinese medicines. Within TCM, even narrower categories appear, such as tonics, pediatric medicines, gynecology-related products, and gastrointestinal treatments. In medical devices and in-vitro diagnostics (IVD), markets are usually defined by product type or technological pathway (e.g., CT, MRI, ultrasound, DSA, electrophysiology, vascular intervention, radioimmunoassay and chemiluminescent immunoassay reagents, and energy-based devices). In pharmaceutical distribution, “wholesale” and “retail” are often treated as distinct relevant markets, and are frequently analyzed in conjunction with upstream manufacturing markets in vertical contexts.

B. Definition of Relevant Geographic Market

Geographic definition reveals a structural distinction between upstream and downstream segments. Drug and device manufacturing/supply markets are generally defined as national in scope, reflecting standardized regulation and smooth inter-regional distribution. By contrast, healthcare service markets (general hospitals, specialty hospitals, pediatric or obstetrics clinics) and retail pharmacy markets are often defined at the city or prefecture level, corresponding to patient catchment areas, reimbursement boundaries, and the local competitive landscape. While wholesale markets are typically treated as national, SAMR frequently defines downstream retail or service markets simultaneously in vertical analyses, and these are usually confined to specific cities or regions. In a small number of cases involving cross-border supply or highly tradable inputs—such as certain sensors, contract research organization (CRO) services, or contract development and manufacturing organization (CDMO) services—the relevant market has been defined globally, though such examples remain rare in healthcare merger reviews.

C. Emerging Business Models and Digital Health: Tend to Be Treated as Independent Markets

Sectors such as internet hospitals, third-party testing services, healthcare IT systems, and third-party logistics for drugs and devices have appeared with increasing frequency in recent cases. Regulators generally adopt a cautious “separation” approach: internet hospitals are treated as distinct from offline healthcare services; healthcare IT system development is independent of both device distribution and hospital services; and third-party logistics is assessed separately from pharmaceutical wholesale markets.

Overall, China’s merger control practice in healthcare shows three notable features. First, product markets are highly granular, typically segmented by therapeutic indication or device type. Second, geographic markets diverge between upstream (nationwide) and downstream (city-level) segments. Third, many recent transactions span multiple stages of the value chain—production, distribution, retail, and healthcare services—requiring regulators to define and assess several related markets in parallel.

III. Conclusion: Key Regulatory Takeaways and Filing Considerations

The Pharmaceutical Guidelines emphasize that merger reviews in this sector involve a multi-factor assessment. Beyond market shares, SAMR examines the parties’ R&D and innovation capacity, control over distribution channels, marketing authorization (MA) qualifications, and access to pharmaceutical data. Particular weight is given to potential foreclosure risks in vertical deals, barriers to market entry, and the transaction’s impact on drug diversity, availability, and pricing. The Guidelines also highlight that APIs, pipeline products, and IP-intensive transactions may raise specific concerns, given their potential to constrain downstream production or technological progress.

Importantly, transactions falling below the statutory filing thresholds are not immune from scrutiny. Where evidence suggests that a deal may eliminate or restrict competition, SAMR may require a filing or even initiate an ex officio investigation. As illustrated by the conditional clearance of Simcere/Tobishi and the prohibition of Wuhan Youtong/Shandong Huatai, the regulator has shown a willingness to look beyond formal thresholds and conduct substantive competition analysis. This underscores that merger compliance risks in healthcare go beyond the traditional question of filing thresholds and instead require forward-looking assessments of potential competitive effects at the deal-planning stage.

For companies, three compliance priorities stand out. First, beyond horizontal overlaps, careful attention must be paid to vertical and conglomerate or cross-market transactions, where risks of supply chain foreclosure, channel dependence, or cross-market bundling are often central to review. Second, high concentration in specific therapeutic indications or local retail/healthcare service markets can trigger heightened concerns. Third, emerging areas such as internet hospitals, third-party testing, healthcare IT, and digital health solutions, though innovation-driven, are often treated as independent markets and thus carry their own compliance risks. For leading corporates and investment funds, early engagement with SAMR, proactive structuring, and preparation of workable remedies may prove decisive for obtaining clearance and achieving successful integration.